When faced with pension decisions, how do you know what is best for your circumstance? Understanding how your pension benefit works will help you plan for your future.

What is a pension?

A pension is simply a source of income that you draw during your retirement. There are two main types of pension plans: Defined Benefit Plans (DB Plans) and Defined Contribution Plans (DC Plans). This article will focus on Defined Benefit Plans.

The Basics

A Defined Benefit Plan is simply that. At the outset of the plan, the plan sponsor (an employer, government, or union) defines what annual benefit they promise to pay for the duration of your retirement according to a specific formula.

How much benefit will I receive?

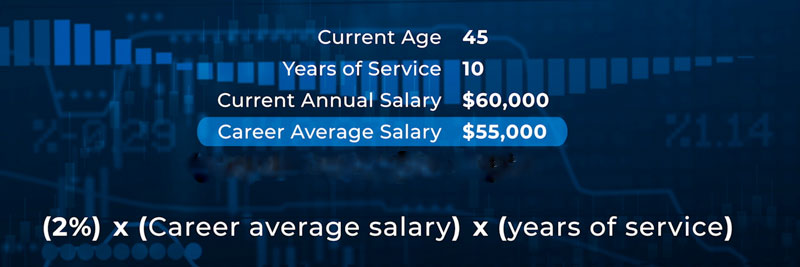

You will accrue, or build up, your retirement benefit according to the plan’s predetermined formula which vary between pension plans. Let’s illustrate this with an example of a common pension formula. For example, your pension statement will probably list some information like:

A common formula for an annual retirement benefit at age 65 = (2%) x (Career Average Salary) x (Years of Service)

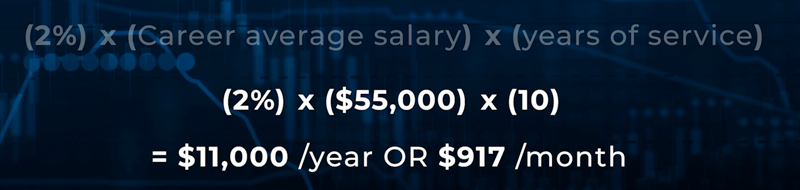

The benefit you’ve earned or accrued up until this point is:

Current accrued annual retirement benefit at age 65 = (2%) x ($55,000) x 10 = $11,000/year OR $917/month

Your accrued benefit has already been promised. Even if you didn’t work another day at the company, this benefit would be owed to you.

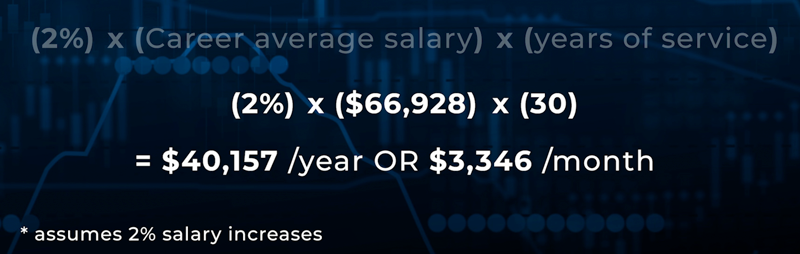

The statement may also show a projection of what your benefit would be if you continued to work until 65 receiving regular salary increases.

Estimated annual benefit at age 65 = (2%) x ($66,928) x 30 = $40,157/year OR $3,346/month

The defined benefit amount would be adjusted for early or late retirement. Your pension plan administrator can provide estimates of your pension values at specific retirement dates.

Exit Strategies: What if I leave the pension plan before retirement?

Taking a lump sum benefit (Commuted Value)

Generally, you will have the option to take out your retirement as a lump sum benefit payment (called a commuted value) if you are under the age of 55.

The lump sum payment is calculated so that if you invested the money personally, you would be able to fund an equivalent retirement benefit for yourself. A large portion of this lump sum is required to be transferred into a locked-in account with withdrawal restrictions so that the money is earmarked for retirement. The remainder will have to be received in cash and taxed as income which can create a high tax bill for the year it is received.

Taking the monthly pension

Once the retirement date is known, the plan will calculate your retirement benefit based on the plan’s defined formula, and you will be offered different options for payout. Reviewing payout options can be overwhelming but it’s important to remember that these options are calculated to be actuarially equivalent, meaning statistically they would cost the same. Deciding on the best option will be unique to your situation. Some common options are as follows:

Life only benefit

- Offers the highest monthly benefit

- Only pays for the duration of your lifetime

Guarantee period

- If you die within the guarantee period the plan will pay out the remaining payments within the guarantee period to your spouse or beneficiary

- If you outlive the guarantee period, the pension will cease at your death just like the life-only benefit

Joint and Survivor benefits

- Payments continue to your spouse after your death until your spouse’s death

- Only available to spouses or common law partners, not other beneficiaries

Bridge benefits

- Available when retiring earlier than 65 where the pension plan pays a higher amount up until age 65 (the bridge) that then drops off to a lower amount when other government benefits such as CPP and OAS would normally kick in

All benefits are taxed as income when received. This form of pension income can be split between spouses prior to age 65.

A Financial Planner can help

Defined Benefit Pension Plans should be appreciated for what they are – a benefit promised to you based on a defined formula. Whether you find yourself in the accruing stage of your pension or deciding on how to draw your benefit, a financial planner can help bring clarity and help you to make decisions that work best for your specific circumstance taking into context your entire financial world.